Team lxme

Traditionally, women love to buy gold on the occasion of Dhanteras or Diwali. Till now, you might be investing in gold physically but not this Diwali!!

Let’s invest smartly this Diwali!!

Gold may not be a great builder of wealth but its ability to maintain value over centuries makes it remarkable. But does this mean you should start hoarding gold jewellery?

– We often tend to believe that gold jewellery is an investment. However, we neglect the liabilities that gold jewellery, or physical gold, for that matter, brings.

– Not to forget, the fear of theft is inevitable. Gold jewellery is a luxury and is consumed and hence, can not be categorized as an investment.

– Gold jewellery or physical gold comes with a huge markup. And there are various additional costs involved such as you have to pay 3% GST on purchases, Storage costs, Insurance costs, making charges, and design charges.

– These additional costs are impossible to recover while selling any gold jewellery. Thus, while painting the bigger picture we realise how gold jewellery is a big NO.

– Some investors often mistake physical gold as an investment option too. You may think that gold coins and bullions don’t fetch making and design changes, but we can’t ignore the storage and protection charges, and the GST that follows.

It’s time to go Digital!

– In today’s time, if you are a smart investor, you will realize the benefits that you can enjoy by investing in gold electronically.

– It’s hassle-free, fairly valued, and a pure form of investment. Although, there are various ways of investing in Gold electronically, and having choices is great but it does lead to confusion. Here’s your go-to guide to investing in gold electronically!

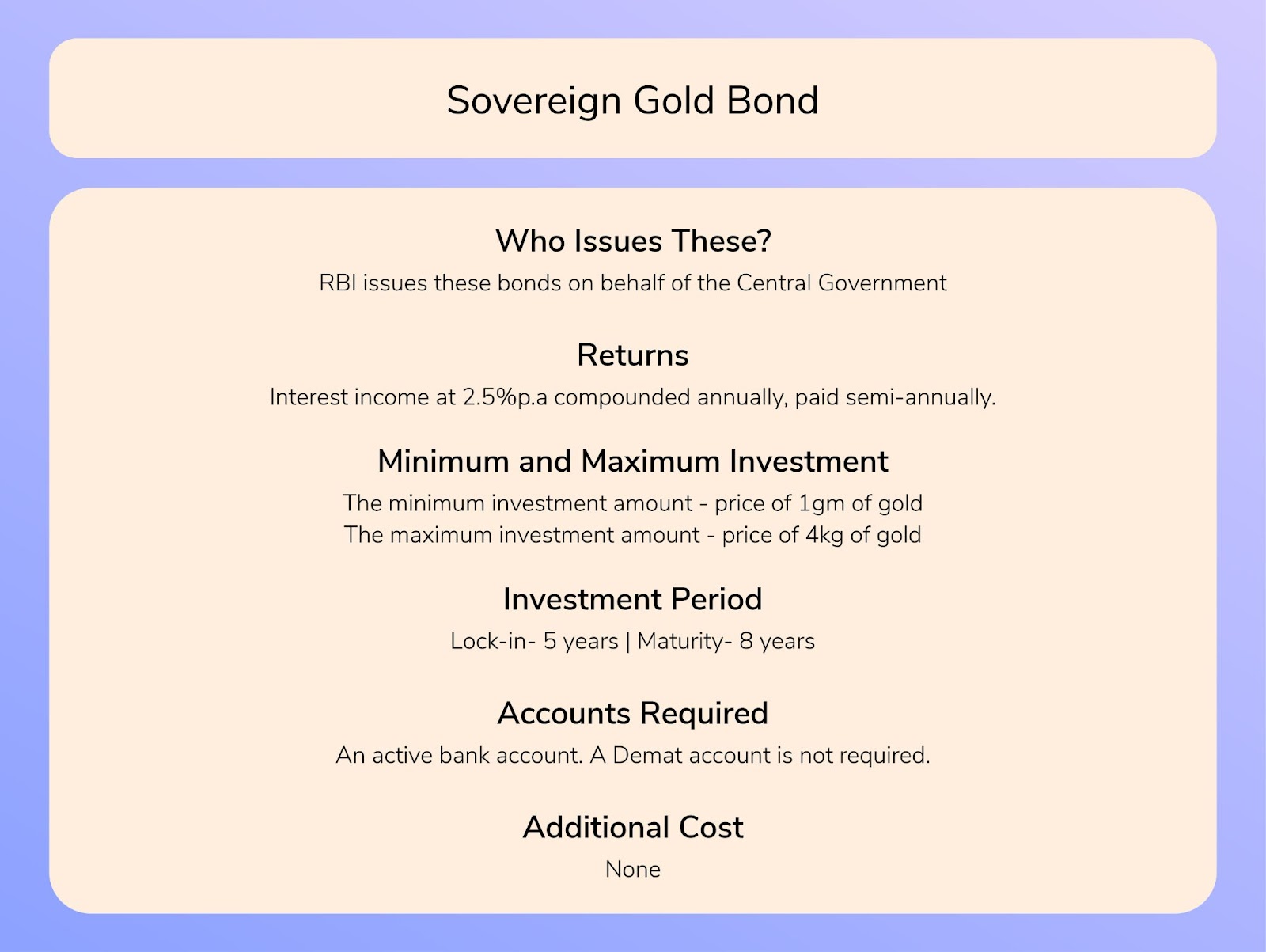

Sovereign Gold Bond

– Sovereign Gold Bonds are RBI-mandated certificates issued against grams of gold and are regarded as one of the most lucrative ways of investing in gold.

– Your investments get 2.5% of interest over and above the capital gains.

– An added bonus is that investors of SGB do not have to pay a capital gains tax on the maturity of this instrument if it is bought through primary issuance.

-So if you are looking at making a lump sum, long-term investment in gold with an added interest income of 2.5% per annum, SGB is for you!

Gold Mutual Fund

– These are mutual funds that directly or indirectly invest in gold.

– Gold Mutual Funds invest in the shares of gold mining and distribution companies, physical gold, and Gold ETFs. It is a convenient way to invest in an asset without having to purchase the commodity in its physical form.

– Gold Mutual Funds are suitable for investors who want to make small investments in gold or are looking for a short-term investment option. You can also make regular investments in Gold Mutual Funds by starting a SIP.

Click here to start investing!

Gold Exchange Traded Funds (Gold ETFs)

– These are exchange-traded instruments that invest in 99.5% pure gold. None of the taxes levied on physical gold purchases are applicable to this investment instrument which also happens to offer safety and efficiency at the same time.

– Gold ETFs are listed and traded on the National Stock Exchange of India (NSE) and Bombay Stock Exchange Ltd. (BSE) like any company’s stock and can be bought and sold continuously at market prices.

– These are ideal for investors who are looking for ultra-short-term investment/trade options or are looking for an investment that offers easy liquidity.

There are also Digital Gold Plans/e-gold plans are also available in the market where you can buy gold for as little as Rs.1/-. But remember, Digital Gold does not come under the purview of any financial regulator therefore, one needs to select the platform carefully.

Tax Implications on Gold

The tax implication mostly remains the same across instruments.

– If you are invested in Gold and you sell this then the following taxation will be applicable:

Short-Term Capital Gain: If the holding period is < 36 months, then tax will be as per your slab rate.

Long-Term Capital Gain: If the holding period is >36 months, then tax will be applicable at the rate of 20% with indexation benefits along with a surcharge(if applicable) and cess of 4%.

– Only in the case of SGBs, the above-mentioned tax implications sustain if the instrument is sold after 5 years but before 8 years. Besides, If you stay invested till the maturity period of 8 years, the capital gains are tax-exempted however, interest income is taxed as per your slab rates.

Gold is a safety net that you must incorporate into your portfolio. So, invest in intrinsic gold like Gold Mutual Funds, Gold ETFs, or Sovereign Gold Bond;

that will keep you away from fools’ gold.

Let’s Smartly invest in Gold this Diwali!!!

Comment “✋” how many of you invest in gold on the occasion of Dhanteras or Diwali

Please note, The Lxme Dream Card services has been discontinued from 30th November, 2024 to make way for something very exciting!

Sorry for the inconvenience caused and stay tuned for something really special!

New Investor? Request a Callback.

Fill in your details and we will guide you at every step

other blogs

Gold January 23, 2025

Expert Tips on How Much of Your Portfolio Should Be in Gold?

We all know that investing in gold is very essential as it’s timeless, reliable, and is a great diversifier. But when it comes to actually investing, one question always pops up in our head is “How much should I invest in gold?” Should it be all my money, or just a part of my investment … Expert Tips on How Much of Your Portfolio Should Be in Gold?

By Siddhi Sharma, CFP®

Gold November 19, 2024

Why Gold Investing is a Smart Choice for Long-Term Wealth

Traditionally or emotionally gold has always held a special place in women’s hearts. For many of us, gold is not only beautiful yellow metal but also meaningful. Whether it’s passed down as a family heirloom, bought for a festive occasion, or simply as a gift to ourselves, gold holds sentimental and financial value. But gold … Why Gold Investing is a Smart Choice for Long-Term Wealth

By Siddhi Sharma, CFP®

Gold October 31, 2024

7 Interesting Facts About Gold

Gold, the shiny yellow metal holds a special place in every woman’s life, from the jewelry handed down by our grandmothers to that special piece we buy to mark life’s big moments & wins. However, gold is not just a symbol of beauty and security but also it has a rich history, unique qualities, and … 7 Interesting Facts About Gold

By Siddhi Sharma, CFP®