Team lxme

Welcome to a wealth-building journey that lasts a lifetime! In our latest blog, ‘How to Build Long-Term Wealth’ on Lxme, we unravel the strategies for sustained financial success. Explore practical insights and expert advice to kickstart your path to long-term wealth creation. Let’s embark on this journey together, shaping a prosperous future.

Presently, the tendency of younger people who have just embarked on their professional journey is to spend money and enjoy their lives, fulfilling their desires with their own money as they become financially independent.

However, this leads to exhaustion of your money and no buffer for your future life goals. With the increasing rate of inflation, just saving your money is not an option as with time your savings will drain out. Hence, an individual should look for options that can save your money as well as eventually grow your money into wealth, which will aid you in satisfying your goals.

Why is long-term investment important for women?

Every girl wants her life to be dreamy after she starts earning and becoming financially sane. Buying various amenities for herself is a distinct satisfaction, but to continue a moral standard of living finances is very important. Without adequate planning for finances, it is unfeasible. Wealth creation is creating an abundance of money in life so that she fulfils every goal she has ever dreamt of.

Every woman carries a bag of responsibilities her whole life such as weddings, day-to-day family responsibilities, children’s upbringing, education, etc. these responsibilities need finances in place in order to carry on life smoothly with no interruption.

Women are masters of budgeting and saving money for the future. However, in order to survive in this inflation-bearing world, just saving is not sufficient. You need to invest and grow your money. For ages, women depend on men for financial security but with time it’s changing as women are educating themselves and they have started to earn for themselves and their families.

However, many of them are still unaware of the fact of investing. As per Lxme’s survey, 51% of women are either not investing their money at all or not aware of the investments in their name and 73% of women were saving less than 20% of their income. So, how to create wealth? Here it is!

How to create Long Term Wealth ?

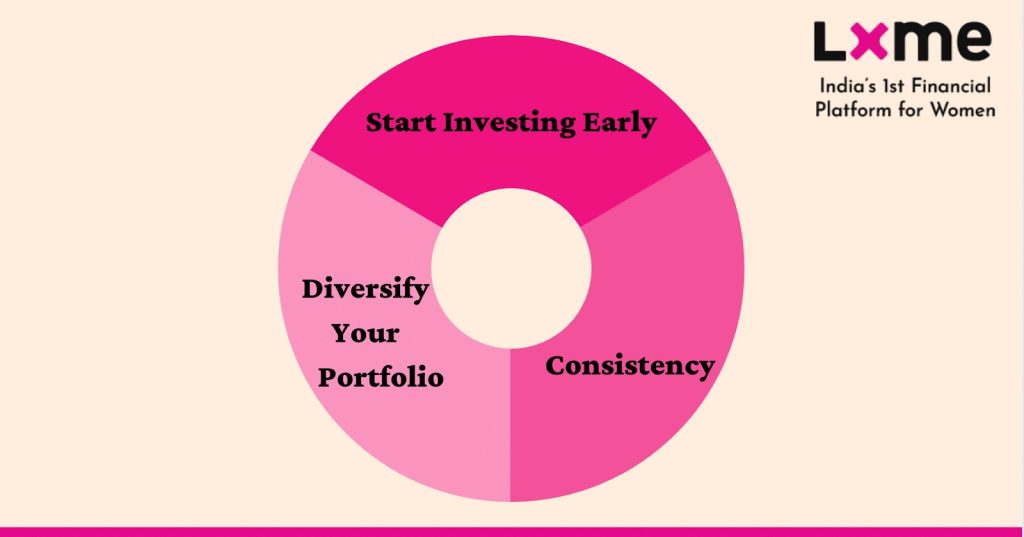

Investing is growing your money and understanding how to increase wealth over a longer period of time. The paramount purpose of investing is generating returns which, in turn, will create wealth by increasing the value of the investment. Wealth Creation is not an easy task as it requires a sacrifice of some present money or asset you own, effort, patience, and time. Every woman should follow 3 wealth creation strategies given below.

- Start Investing Early: Investing early in life aids in saving more than compared to those who start investing in later stages of their life. Even small amounts can do miracles in the long term.

- Consistency: While investing, one should be patient and consistent to reap optimal benefits. Be a saver, not a spender. This will enable you to have a habit of saving in any circumstance which will lead to creating a significant amount of wealth.

- Diversify your portfolio: The saying “Don’t put all your eggs in one basket” goes well here. As markets are volatile in nature, one should invest in different investment avenues to get stable returns on your portfolio.

Let’s have a look at an example of how you can create wealth in long term:

Radha and Aarti are two friends who embarked on their working life journey at the age of 22. Both earn Rs. 25,000 every month. Radha and Aarti both have different perspectives on their life. Radha believes in investing her money to fulfil her future goals, long term wealth creation as she is well informed about the advantages of early investing. So, Radha starts her investment journey right away as soon as she receives her first salary with Lxme Long Term Plan for Rs. 5,000 per month at the rate of 14% till her retirement, i.e. till age 60.

On the other hand, Aarti believes in enjoying her life to the fullest and spending on different luxuries. She thinks her whole life is ahead to invest and doesn’t focus on how to increase wealth so she ends up spending all her salary up to the time she realised the importance of investing. She asks Radha for a good fund she can invest in her money and reap the benefit she is receiving. Radha suggests Lxme’s Long term Plan and starts investing in the same from age 27 with Rs. 5,000 at the rate of 14% till her retirement i.e. till age 60. So let’s look at what corpus Radha and Aarti have accumulated at the age of 60.

Evidently, we can see the power of compounding in the longer term. Radha was able to accumulate ₹ 4.30 crore (₹ 8.54 crore – ₹ 4.24 crore) more than Aarti, as Radha just started 5 years earlier. To match the corpus of Radha, Aarti will have to invest Rs. 10,079 at the rate of 14% or will have to invest Rs. 5,000 at the rate of 16.66%. If you invest early, even small amounts of investments with consistency can make you millionaires.

Where can you invest your money in wealth creation?

Investment in different avenues varies from person to person according to the risk appetite, investment horizon, corpus targeted, frequency of investment, and goals. There are various investment avenues such as equity, debt, and gold.

To create wealth, one can devote a sizeable chunk to Equity as it acts as a value creator in the portfolio. Investing in direct equity can be quite risky as she should possess adequate knowledge about the same and have a high-risk appetite. If you do not possess the right knowledge about investing in direct stocks, then you might end up losing all your money.

So, it is better to invest in equity through Equity Mutual Funds as it offers flexibility as well as diversification. Mutual funds are being managed by professionals, who are better equipped and trained to manage money. They will diversify your money among various instruments and try to provide you with a capital gain or returns to the investor at a lower cost.

Investment in equity aids investors in receiving inflation-beating returns, which is why it is important to have equity exposure in your portfolio.

Along with this, investors can allocate some proportion of money towards Debt/Fixed Income Securities for the stability of the portfolio. Investors with a lower risk appetite can invest in Debt Mutual Funds. Debt funds are funds that are less volatile than equity funds.

These funds invest in debt instruments like commercial papers, government securities, treasury bills, corporate bonds, and other money market instruments. Investors with a lower risk capacity choose to invest in these types of funds.

Lastly, fixed income securities such as Post Office Savings Schemes, Public Provident Fund, gold, etc. can help you receive fixed income with no risk. Investors can also allocate 5-10% of their portfolio to gold as it hedges the portfolio against inflation and market volatility.

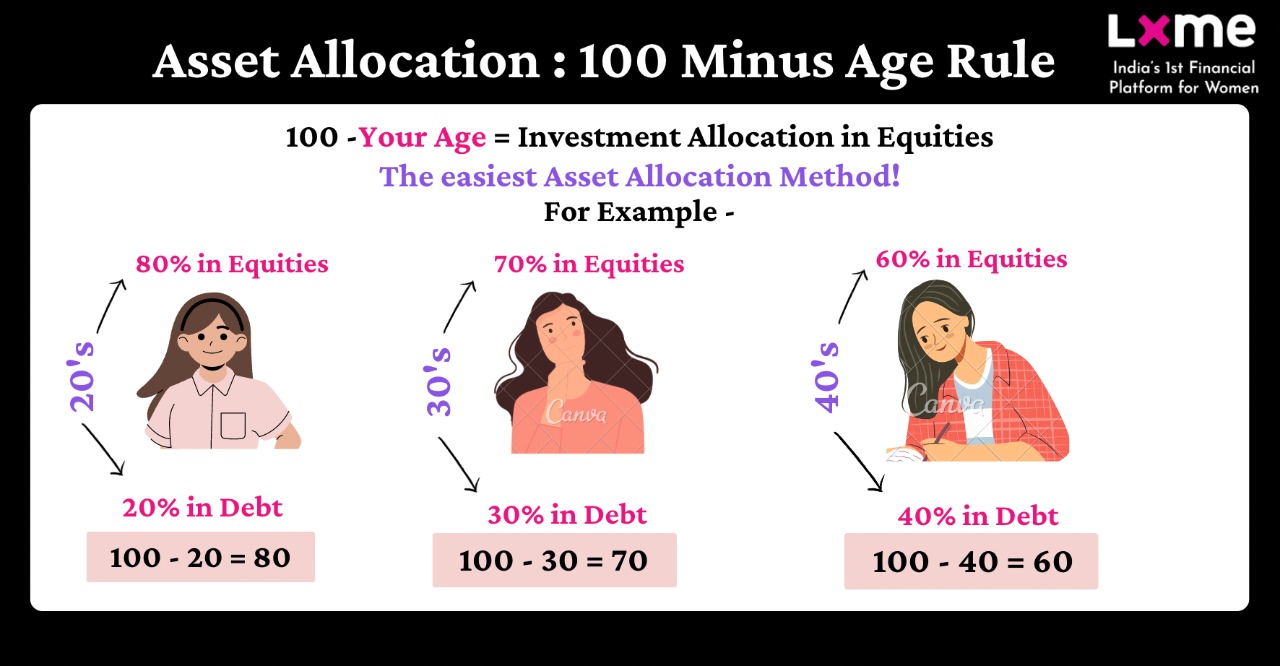

Asset Allocation

Generally, the risk appetite of younger investors is quite high as they are ready to take up risk and bear the same so they can allocate a higher proportion of their assets towards equity and the remaining part towards debt and fixed-income securities. As investors get older, their risk appetite falls, the equity proportion falls, and the debt and fixed income proportion increases. As her retirement risk appetite falls down, she looks to invest in low-risk instruments or risk-free instruments.

You can follow the Asset Allocation by Age Formula:

It says that 100-Age=Investment Allocation in Equities

To conclude, currently, both men and women should possess adequate financial plans to have a peaceful life. Life is full of uncertainty. No one can predict any mishap, so one should plan their finances beforehand. In long term investing diversification is the key to stable returns on your portfolio. You can have a mix of the above-mentioned investment avenues along with gold investment which can provide you diversification in your portfolio. Too risky and too low-risk portfolios don’t offer optimal returns on portfolios and can become a drawback for wealth creation that is why one should have a mix of both risky as well as low-risk investment avenues.

If you found this helpful, share this blog with your friends and family!!

Download the Lxme app now to start investing!

Related Article You May Like: – Wealth Personality Test: Customizing Debt Payoff Strategies

FAQs – Common Questions on Long Term Wealth Creation

How should we have a mix of different investment avenues in our portfolio? What should we consider before adding it to the portfolio?

The mix of investment avenues can be decided based on how much risk you are ready to take, if you have a high-risk appetite then equity proportion will be higher in your portfolio, for instance, 70%, debt or low-risk investment avenues will be lower i.e. 20% and fixed income investment avenues will be remaining part of your portfolio i.e. 10%.

In the same way, you can plan for a lower risk appetite as well as a moderate risk appetite individual. This is how you can reap optimal returns on your portfolio over a longer period of time.

What does a financial plan mean?

A financial plan is a broader concept as it consists of various components such as insurance planning in order to protect your life from any sudden mishap, investment planning in order to fulfil day-to-day goals, retirement planning for peaceful sunset years, tax planning for investing in tax-efficient investment avenues in order to save tax and lastly estate planning in order to bequeath the wealth of individual after death to legal heirs. However, an individual must possess a financial plan for a peaceful financial life.

Minimum how many years we should invest in wealth creation?

One should invest at least 8 to 10 years to reap benefits and create wealth.

How are equity investments taxed?

Short Term Capital Gain: Investments sold and Capital gains arising within 12 months are termed short-term capital gains (STCG). They are taxed at the rate of 15 per cent.

Long Term Capital Gain: Investments sold and Capital gains arising after 12 months are termed long-term capital gains (LTCG). They are exempted for up to Rs 1 lakh. Gains in excess of Rs 1 lakh are taxed at the rate of 10 per cent without indexation.

Mutual fund investment is simple. Here are some steps to learn and know where to start. ⬇⬇

To stay connected with Lxme and access inspiring content, follow us on Instagram and subscribe to our YouTube channel.

Please note, The Lxme Dream Card services has been discontinued from 30th November, 2024 to make way for something very exciting!

Sorry for the inconvenience caused and stay tuned for something really special!

New Investor? Request a Callback.

Fill in your details and we will guide you at every step

other blogs

Mutual Funds June 21, 2025

Are Gold Mutual Funds a Good Investment in 2025? Pros and Cons Explained

Gold has always had a special place in Indian hearts, especially every woman’s heart, be it weddings, festivals, gifts from our moms, or just for investment. But today, women are not just buying gold for jewellery. We’re also thinking about how to grow our money smartly, right? And that’s where Gold Mutual Funds come in! … Are Gold Mutual Funds a Good Investment in 2025? Pros and Cons Explained

By Siddhi Sharma, CFP®

Money Hacks May 21, 2025

How to Apply for Mahtari Vandana Yojana: Step-by-Step Process

The Mahtari Vandana Yojana launched by the Chhattisgarh government aims to promote the economic self-reliance of women in the state while ensuring continuous improvement in their health and nutrition levels. It seeks to strengthen their decisive role within the family, remove discrimination and inequality, and address the lack of awareness about women’s rights in society. … How to Apply for Mahtari Vandana Yojana: Step-by-Step Process

By Siddhi Sharma, CFP®

Mutual Funds March 28, 2025

How To Invest in Gold Mutual Fund Through SIP?

Women and gold share a deep bond for ages. Traditionally, buying gold jewelry or physical gold in the form of bars, coins, etc. has been seen as a form of investment. But times have changed & evolved, so we need to evolve too! Now, you can invest in gold without physically owning it, with no … How To Invest in Gold Mutual Fund Through SIP?

By Siddhi Sharma, CFP®