Let’s be honest, most financial advice wasn’t written with women investors in mind. It assumes you have a steady income from day one, no career breaks, no salary gaps, and no caregiving responsibilities. Real life is messier than that.

The good news? Two of the most powerful investment methods, SIP and lump sum, can be shaped around your life, not the other way around. Let’s understand both clearly.

What is a SIP?

SIP stands for Systematic Investment Plan. In simple terms, it means investing a fixed amount, say ₹1,000 or ₹5,000, every month into a mutual fund, automatically. Think of it like a gym membership for your money. A small, consistent effort that builds results over time. You don’t need to watch the market. You don’t need a large amount upfront. You just set it and let it grow.

Here’s the magic part: SIPs use something called rupee-cost averaging. When the market is low, your fixed amount buys more units. When it’s high, it buys fewer. Over time, this averages out your cost and often gives better returns than trying to time the market.

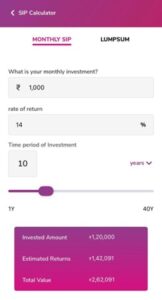

For example, if you invest ₹1,000 every month for 10 years at an assumed 14% return, your total investment of ₹1.2 lakh could grow to around ₹2.62 lakh. You can calculate your amount now using this link https://lxme.onelink.me/95JV/calculator1

What is a one-time (lump sum) investment?

A lump-sum investment means putting a large amount of money all at once into a mutual fund, stock, FD, or any investment vehicle. You invest once and let it grow over time. This works beautifully if you’ve received a bonus, sold a property, received an inheritance, or have savings sitting idle in a low-interest account. Instead of letting it sleep, you put it to work. https://lxme.onelink.me/95JV/LumpsumCalculators04

The real difference between the two

Here’s your content structured into a clean table:

| Feature | SIP (Monthly) | Lump Sum (One-Time) |

| Best for | Investor with regular income | Investors with surplus funds or windfalls |

| Mode | Fixed amount invested at regular intervals | The entire amount is invested at once |

| Pros |

|

|

| Cons |

|

|

| Behavioural benefit | Encourages discipline and consistency | Requires emotional comfort with volatility |

There’s no single winner. The best choice depends entirely on your life stage, income, and goals. Which brings us to the most important part.

How to get started today

Step 1: Open your account—Sign up on the Lxme app and complete your KYC with PAN and Aadhaar in minutes.

Step 2: Choose a fund type based on your goal, risk appetite, and time horizon

For example, use equity funds for long-term growth, debt funds for stability, and balanced funds for a mix of both.

Step 3: Set your SIP date — Pick a date just after your salary comes in and automate it.

Step 4 Start small—even ₹500 or ₹1,000 is enough. Consistency matters more than the amount.

Step 5 Review once a year—check yearly, not daily. Increase your SIP when you can.

Step 6 Stay invested in market crashes—don’t stop. You buy more units at lower prices, which helps in the long run.

Is Combining SIP and Lumpsum a Good Strategy?

Yes, combining both SIP and lump sum is a good strategy to earn better returns in the long term. You can invest a part as a lump sum so the money starts compounding immediately and put the rest through SIP or STP to spread your entry over time. This reduces timing risk while keeping your investments disciplined, especially for long-term goals.

For example, if you have ₹5 lakh today but invest ₹20,000 monthly, you can invest part as a lump sum and route the rest via SIP. This balances immediate market exposure with disciplined investing and is commonly used in long-term wealth management strategies.

Tax Treatment of SIP vs Lumpsum

Taxation depends on the type of mutual fund, not the investment method.

SIP and lump-sum investments follow the same tax rules:

- Equity funds: Long-term gains after one year are taxed at 12.5% (above ₹1.25 lakh yearly gains). Short-term gains are taxed at 20%.

- Debt funds: Gains are taxed at the investor’s income tax slab rate.

Each SIP installment is treated as a separate investment for tax calculation.

Things to Consider Before Investing

- Cash flow is the first factor to consider. SIP suits investors with regular income, such as salaried professionals, because it allows small, periodic investments. A lump sum works better if you have idle or surplus cash available upfront.

- Financial goals influence the investment method. SIPs are suitable for long-term goals such as wealth creation, retirement, or children’s education. A lump sum is useful when you want to deploy idle cash into equities rather than keeping it in low-return options like savings accounts or fixed deposits.

- Fund type plays an important role. Equity funds are volatile, making them suitable for SIPs, as regular investing helps manage market ups and downs. Debt funds are less affected by market movements, so returns from SIP and lump-sum investments tend to be similar.

- Time horizon also matters. A longer investment period reduces the impact of market timing and allows compounding to work more effectively.

- Investor behaviour affects outcomes. Staying consistent with investments often matters more than choosing the perfect time or method.

How to Decide Between SIP and Lumpsum

SIP makes sense if you earn a regular income and prefer investing steadily without worrying about market levels. Lump sum works better when you have surplus cash and a long investment horizon, allowing your money to start working right away. In the long run, staying invested consistently matters more than choosing SIP or a lump sum.

FAQs

How does SIP reduce market risk?

A Systematic Investment Plan (SIP) reduces market risk by spreading investments over time, allowing you to benefit from rupee cost averaging and avoid the impact of market timing.

What are the disadvantages of lump-sum investments?

Lump sum investing carries the risk of poor market timing; if you invest a large amount just before a market drop, you may face significant short-term losses and higher volatility exposure.

Can I stop or pause my SIP anytime?

Yes, you can stop or pause your SIP anytime, giving you flexibility to adjust your investments based on your financial situation.

How can I calculate SIP vs. lump sum returns?

You can easily compare SIP and lump sum returns using the Lxme SIP and lump sum calculator to see which option works better for your goals.

Further Read: