Team LXME

When it comes to tax-saving investments, understanding the choices is key. In this comprehensive guide, we delve into the world of “ELSS vs PPF,” helping you make well-informed financial decisions. Equity Linked Savings Schemes (ELSS) and Public Provident Fund (PPF) are both popular options, but which one suits your needs better? Join us as we break down the differences, risks, returns, and tax benefits to empower you in your investment journey in regards to elss vs ppf. #TaxBachaoLXMEBadhao

Do you also struggle while saving tax?

So, let’s learn how to create wealth and save taxes!

Tax planning is a crucial part of financial planning and in India, people are generally attracted to tax-saving instruments such as post office saving schemes, PPF, NPS, etc.

But are all tax-saving instruments delivering you inflation-beating returns?? Or you are just investing in these instruments to save taxes and earning minimal returns??

So let’s learn how to save taxes and earn inflation-beating returns,

Riddhi, Pooja, and Priya are best friends and one day they sat got into a discussion related to tax planning while discussing they discovered that each of them is investing in tax saving instruments but all 3 of them are investing in a different way.

Riddhi is investing in Public Provident Fund (PPF) (has low risk appetite), Pooja is investing in Equity Linked Savings Scheme (ELSS) (has high risk appetite) and Priya is the smart who is diversifying her portfolio against both tax saving instruments i.e. ELSS as well as PPF (believes in spreading her risk).

First, let’s have a look at these investment instruments individually, to break down the debate of PPF vs ELSS.

Equity Linked Savings Scheme (ELSS):

An equity-linked savings scheme or an ELSS fund is the only kind of mutual fund eligible for tax deductions under the provisions of Section 80C of the Income Tax Act, 1961.

Features:

- Tax deductions of up to ₹1,50,000 a financial year under Section 80C

- Lock-in period of 3 years

- No provisions to make a premature exit

- Minimum Investment: varies across fund houses

Why are ELSS Mutual Funds the Best Tax-Saving Option?

- The dual benefit of tax deductions and wealth creation over time

- Option to invest a small amount every month (SIP)

- Better returns than other tax-saving instruments

- The shortest lock-in period of just 3 Years.

- Delivers returns on an average 14-16%* (market linked returns)

*Is market linked returns. Mutual funds are subject to market risks

Can one invest in an ELSS fund through LXME?

Yes! If you want to start investing in the ELSS fund then you can invest through the LXME app. LXME offers Tax Saving Fund is a portfolio mix of ELSS funds, handpicked by our experts for tax saving purpose under the Income Tax Act.

This portfolio is diversified, well-researched and curated by experts.

Public Provident Fund (PPF):

Public Provident Fund (PPF) is one of the long-term investment scheme backed by Government. It is also called as savings-cum-tax savings investment vehicle that enables one to build a retirement corpus while saving on annual taxes.

Features:

- Tax deductions of up to ₹1,50,000 in a financial year under Section 80C of the Income Tax Act.

- Lock-in period of 15 years

- Has provision of premature withdrawal, you can withdraw up to 50% of the amount in your PPF Account after seven years, beginning from the end of the year you made your initial contribution.

- Minimum investment required in a financial year is ₹500.

- Maximum amount you can invest in PPF account is ₹1,50,000 in one financial year.

- PPF offers 7.1% return (These returns gets revised periodically by Government)

Why PPF is one the most popular tax saving investment instrument?

PPF falls under the Exempt, Exempt, Exempt (EEE) regime.

PPF is tax efficient investment instrument that offers tax benefits in all 3 stages of the investment process: investment stage, accumulation stage, and withdrawal stage.

So, now you might have got confused which investment instrument you should choose right? So, let’s have a look at Riddhi’s, Pooja’s and Priya’s investments after 15 years.

- Riddhi is investing ₹1,500 every month in PPF @7.1% for 15 years

- Pooja is investing ₹1,500 every month in ELSS @16%* (targeted return) for 15 years

- And Priya is investing ₹1,050 every month in ELSS which is 70% of 1500 and ₹450 every month in PPF which is 30% of 1500

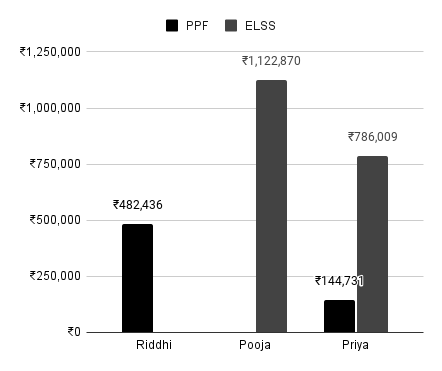

So, let’s have look at what corpus they will accumulate at the end of 15 years in the form of graph:

*16% is targeted return offered by LXME Tax Saving Fund which is market linked

As you can see in the above graph Riddhi was only able to accumulate ₹4,82,436 whereas, Pooja was able to accumulate ₹11,22,870 which is ₹6,40,434 ( ₹11,22,870-₹4,82,436) more than Riddhi.

Riddhi has lower risk appetite so she just invested in PPF while Pooja has higher risk appetite that’s why she invested all of her funds in ELSS. So, what was priya’s approach?

Priya’s approach was to spread risk across two asset classes and enjoy diversification, the power of compounding as well as the tax benefit. She was able to accumulate ₹9,30,740 (₹144,731 from PPF + ₹786,009 from ELSS) at the end of 15 years.

So, now we have seen the difference between two investment instruments. The best practice for investor will be to diversify the portfolio against different asset classes based on your risk appetite. This will deliver inflation-beating returns, ensure stability as well as will give you maximum tax benefit.

If you found this helpful, share this blog with your friends and family!!

Download the LXME app now to start investing!

Related Article You May Like: – Sovereign Gold Bond 2023: Golden Investment Opportunity

FAQs – Common Questions on ELSS vs PPF

1. Is it better to invest in PPF or ELSS?

It depends on your financial goals. PPF offers stability and tax benefits, while ELSS has the potential for higher returns but involves market risks. Choose based on your risk tolerance and investment horizon.

2. Why ELSS is better than PPF?

ELSS has the potential for higher returns due to equity exposure, making it suitable for long-term wealth creation. PPF, while stable, offers lower returns. However, ELSS carries market risks, so assess your risk appetite before choosing.

3. Can I have both ELSS and PPF?

Yes, you can have both ELSS and PPF in your investment portfolio. Many investors opt for a diversified approach, balancing stability with growth potential. Just ensure your investment choices align with your financial objectives.

Find in-depth comparisons in our comprehensive guide about ELSS vs PPF.

4. What is ELSS and PPF?

Elss vs PPF, let’s break it down:

ELSS (Equity Linked Savings Scheme) is a type of mutual fund that primarily invests in equity markets, offering potential high returns with a lock-in period.

PPF (Public Provident Fund) is a government-backed savings scheme with a fixed interest rate, providing a secure and tax-free investment option.

5. Which investment offers better returns: ELSS or PPF?

Generally, another doubt investors face is elss better than ppf or vice versa. Let us understand it better:

ELSS generally has the potential for higher returns due to equity exposure, but it comes with market risks.

PPF offers stable returns, but they are usually lower than ELSS. It prioritizes safety and fixed returns.

6. Which investment is more suitable for long-term financial goals?

For long-term financial goals, ELSS is often preferred as it has the potential to outperform PPF over an extended period.

PPF, being a fixed-income instrument, is more suitable for conservative investors looking for stability in their long-term investments.

SAVE TAX with ELSS Funds | ELSS Funds Explained | LXME Explained ⬇⬇

To stay connected with LXME and access inspiring content, follow us on Instagram and subscribe to our YouTube channel.

New Investor? Request a Callback.

Fill in your details and we will guide you at every step

other blogs

Smart Money April 17, 2024

Bear and Bull Market: What’s the Difference?

In bear markets, prices are falling, investor confidence is low and the economy is declining. While, in bull markets, prices are rising, investor confidence is high and there is good economic growth. You must have heard the terms ‘bullish market’ and ‘bearish market’ on the news. But, what do bear and bull market mean? Is … Bear and Bull Market: What’s the Difference?

By Abhibyakti Singh

Smart Money

What is Udyogini Scheme? Features, Eligibility & Documentations

Financial assistance has the power to transform a woman’s life, especially an underprivileged woman. This is why the Women Development Corporation offers a scheme called Udyogini Yojana to provide women with monetary help in setting up their business. What is the PM Udyogini Yojana Scheme? What are some Udyogini Scheme details? Let’s find out! What … What is Udyogini Scheme? Features, Eligibility & Documentations

By Abhibyakti Singh

Smart Money April 11, 2024

Mahila Udyam Nidhi Scheme: Eligibility Criteria, Interest Rate & More

The Mahila Udyam Nidhi Scheme aims to support women’s entrepreneurial ventures. It is an initiative by the Small Industrial Development Bank of India and offers financial assistance to women entrepreneurs at special interest rates. Women have proven that they can do anything they set their minds to. Against all odds, women are setting up their … Mahila Udyam Nidhi Scheme: Eligibility Criteria, Interest Rate & More

By Abhibyakti Singh